Poster

An Efficient High-dimensional Gradient Estimator for Stochastic Differential Equations

Shengbo Wang · Jose Blanchet · Peter W Glynn

East Exhibit Hall A-C #2500

{kind=link}

Abstract:

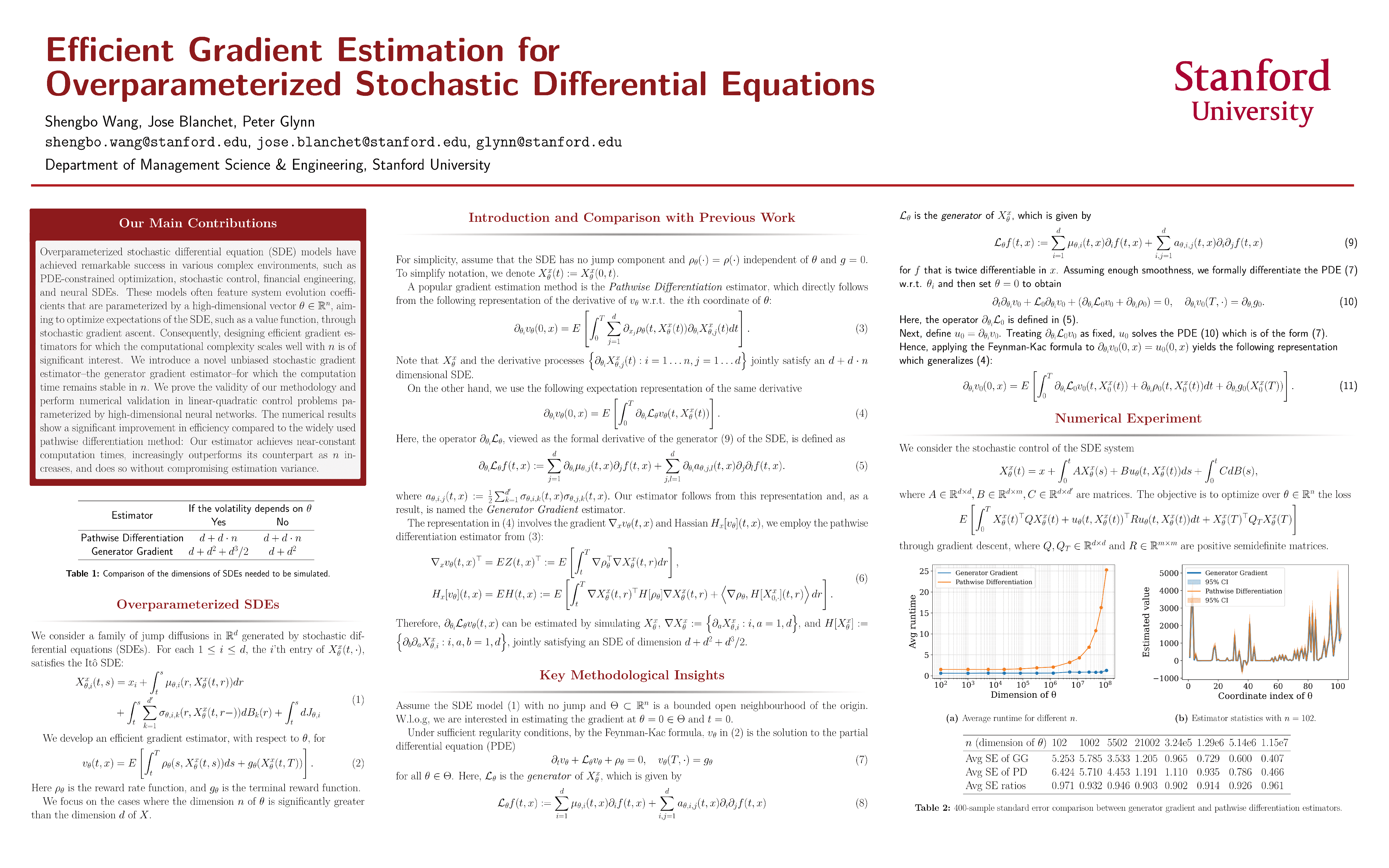

Overparameterized stochastic differential equation (SDE) models have achieved remarkable success in various complex environments, such as PDE-constrained optimization, stochastic control and reinforcement learning, financial engineering, and neural SDEs. These models often feature system evolution coefficients that are parameterized by a high-dimensional vector $\theta \in \mathbb{R}^n$, aiming to optimize expectations of the SDE, such as a value function, through stochastic gradient ascent. Consequently, designing efficient gradient estimators for which the computational complexity scales well with $n$ is of significant interest. This paper introduces a novel unbiased stochastic gradient estimator—the generator gradient estimator—for which the computation time remains stable in $n$. In addition to establishing the validity of our methodology for general SDEs with jumps, we also perform numerical experiments that test our estimator in linear-quadratic control problems parameterized by high-dimensional neural networks. The results show a significant improvement in efficiency compared to the widely used pathwise differentiation method: Our estimator achieves near-constant computation times, increasingly outperforms its counterpart as $n$ increases, and does so without compromising estimation variance. These empirical findings highlight the potential of our proposed methodology for optimizing SDEs in contemporary applications.

Chat is not available.