Poster

TimeXer: Empowering Transformers for Time Series Forecasting with Exogenous Variables

Yuxuan Wang · Haixu Wu · Jiaxiang Dong · Guo Qin · Haoran Zhang · Yong Liu · Yunzhong Qiu · Jianmin Wang · Mingsheng Long

East Exhibit Hall A-C #4306

{kind=link}

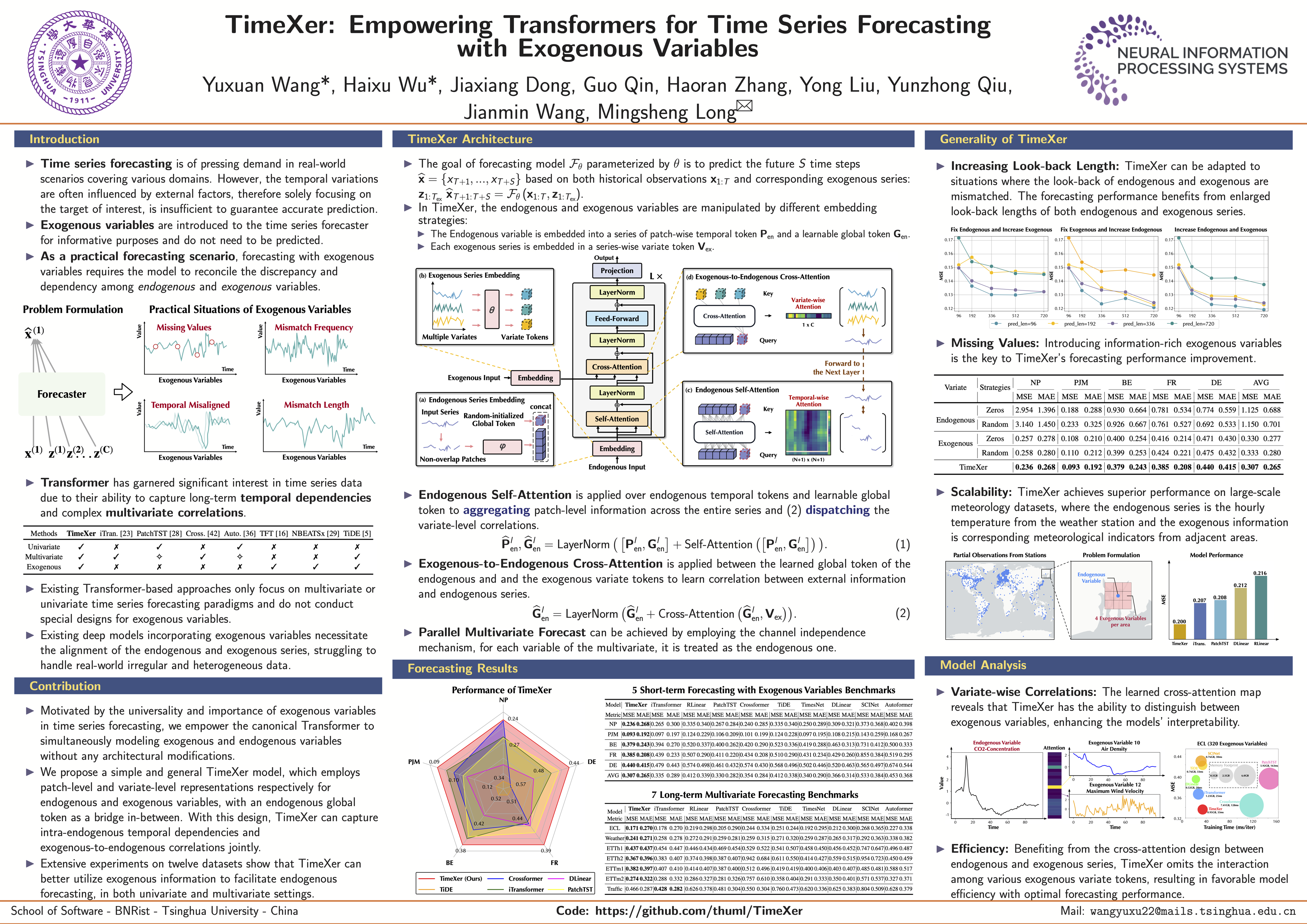

Deep models have demonstrated remarkable performance in time series forecasting. However, due to the partially-observed nature of real-world applications, solely focusing on the target of interest, so-called endogenous variables, is usually insufficient to guarantee accurate forecasting. Notably, a system is often recorded into multiple variables, where the exogenous variables can provide valuable external information for endogenous variables. Thus, unlike well-established multivariate or univariate forecasting paradigms that either treat all the variables equally or ignore exogenous information, this paper focuses on a more practical setting: time series forecasting with exogenous variables. We propose a novel approach, TimeXer, to ingest external information to enhance the forecasting of endogenous variables. With deftly designed embedding layers, TimeXer empowers the canonical Transformer with the ability to reconcile endogenous and exogenous information, where patch-wise self-attention and variate-wise cross-attention are used simultaneously. Moreover, global endogenous tokens are learned to effectively bridge the causal information underlying exogenous series into endogenous temporal patches. Experimentally, TimeXer achieves consistent state-of-the-art performance on twelve real-world forecasting benchmarks and exhibits notable generality and scalability. Code is available at this repository: https://github.com/thuml/TimeXer.