Spotlight Poster

Optimal Algorithms for Online Convex Optimization with Adversarial Constraints

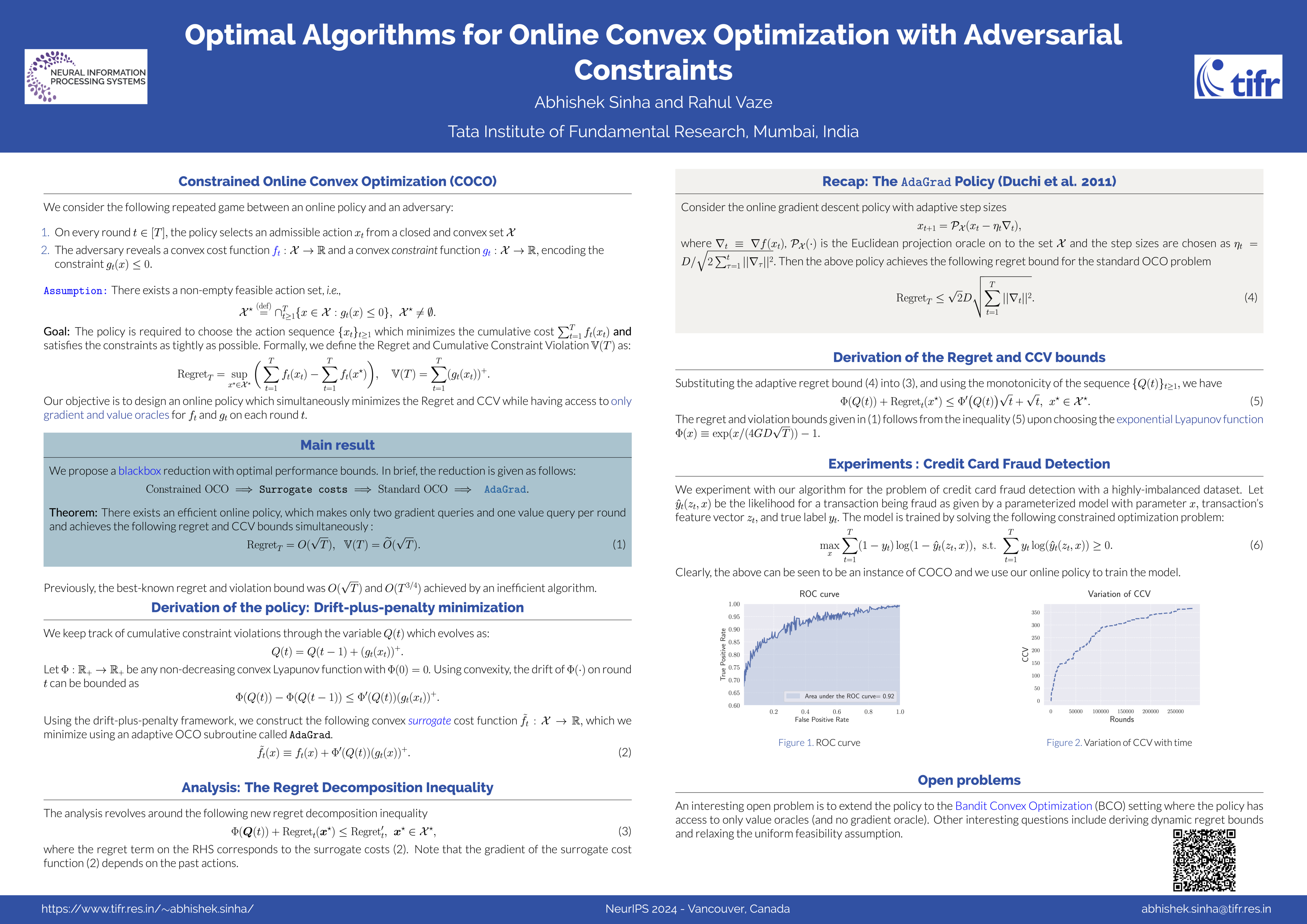

Abhishek Sinha · Rahul Vaze

West Ballroom A-D #7302

{kind=link}

Abstract:

A well-studied generalization of the standard online convex optimization (OCO) framework is constrained online convex optimization (COCO). In COCO, on every round, a convex cost function and a convex constraint function are revealed to the learner after it chooses the action for that round. The objective is to design an online learning policy that simultaneously achieves a small regret while ensuring a small cumulative constraint violation (CCV) against an adaptive adversary interacting over a horizon of length $T$. A long-standing open question in COCO is whether an online policy can simultaneously achieve $O(\sqrt{T})$ regret and $\tilde{O}(\sqrt{T})$ CCV without any restrictive assumptions. For the first time, we answer this in the affirmative and show that a simple first-order policy can simultaneously achieve these bounds. Furthermore, in the case of strongly convex cost and convex constraint functions, the regret guarantee can be improved to $O(\log T)$ while keeping the CCV bound the same as above. We establish these results by effectively combining adaptive OCO policies as a blackbox with Lyapunov optimization - a classic tool from control theory. Surprisingly, the analysis is short and elegant.

Chat is not available.