Poster

Overcoming Brittleness in Pareto-Optimal Learning Augmented Algorithms

Alex Elenter · Spyros Angelopoulos · Christoph Dürr · Yanni LEFKI

{kind=link}

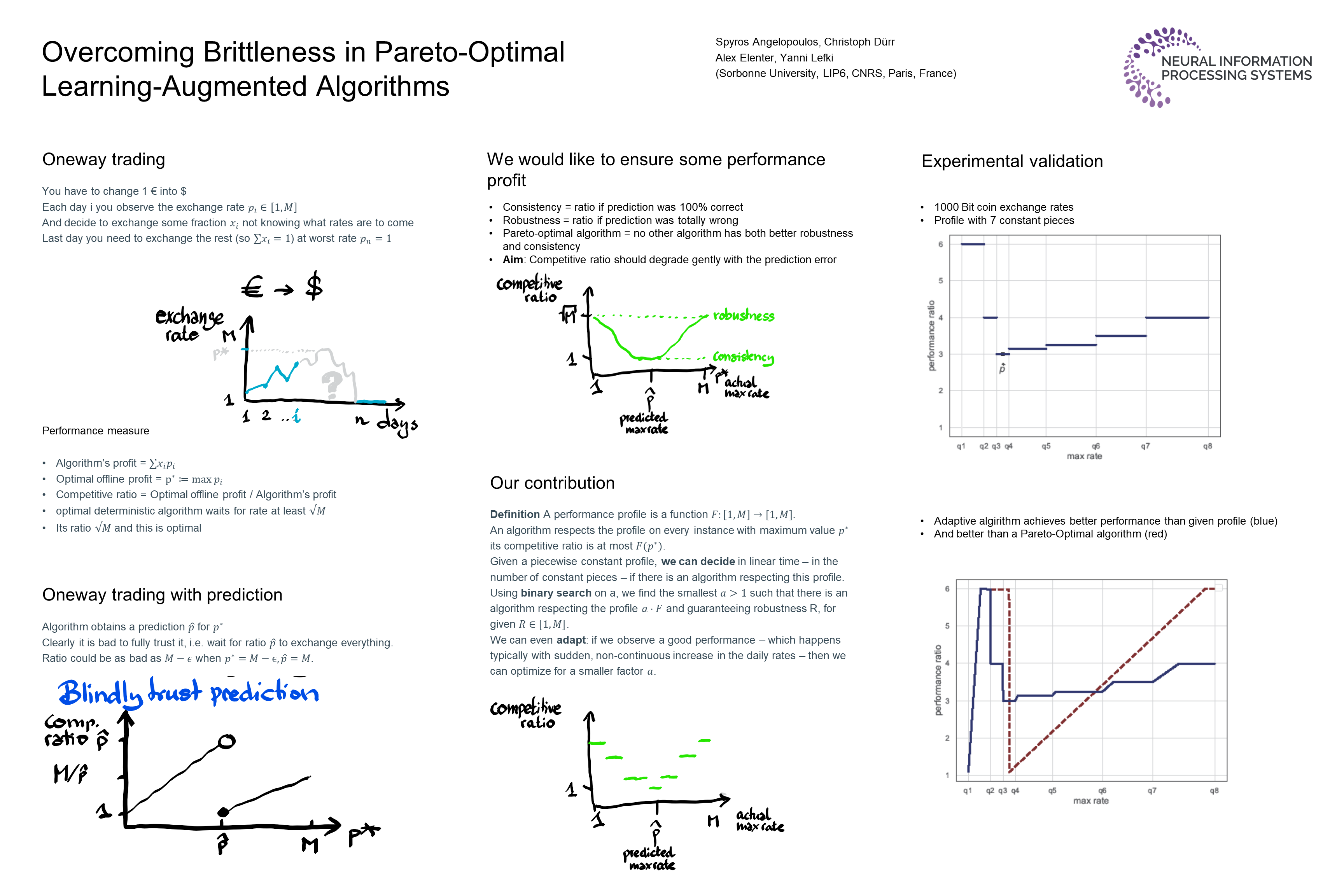

The study of online algorithms with machine-learned predictions has gained considerable prominence in recent years. One of the common objectives in the design and analysis of such algorithms is to attain (Pareto) optimal tradeoffs between the {\em consistency} of the algorithm, i.e., its performance assuming perfect predictions, and its {\em robustness}, i.e., the performance of the algorithm under adversarial predictions. In this work, we demonstrate that this optimization criterion can be extremely brittle, in that the performance of Pareto-optimal algorithms may degrade dramatically even in the presence of imperceptive prediction error. To remedy this drawback, we propose a new framework in which the smoothness in the performance of the algorithm is enforced by means of a {\em user-specified profile}. This allows us to regulate the performance of the algorithm as a function of the prediction error, while simultaneouslymaintaining the analytical notion of consistency/robustness tradeoffs, adapted to the profile setting. We apply this new approach to a well-studied online problem, namely the {\em one-way trading} problem. For this problem, we further address another limitation of the state-of-the-art Pareto-optimal algorithms, namely the fact that they are tailored to worst-case, and extremely pessimistic inputs. We propose a new Pareto-optimal algorithm that leverages any deviation from the worst-case input to its benefit, and introduce a new metric that allows us to compare any two Pareto-optimal algorithms via a {\em dominance} relation.