Poster

A Globally Optimal Portfolio for m-Sparse Sharpe Ratio Maximization

Yizun Lin · Zhao-Rong Lai · Cheng Li

West Ballroom A-D #6009

{kind=link}

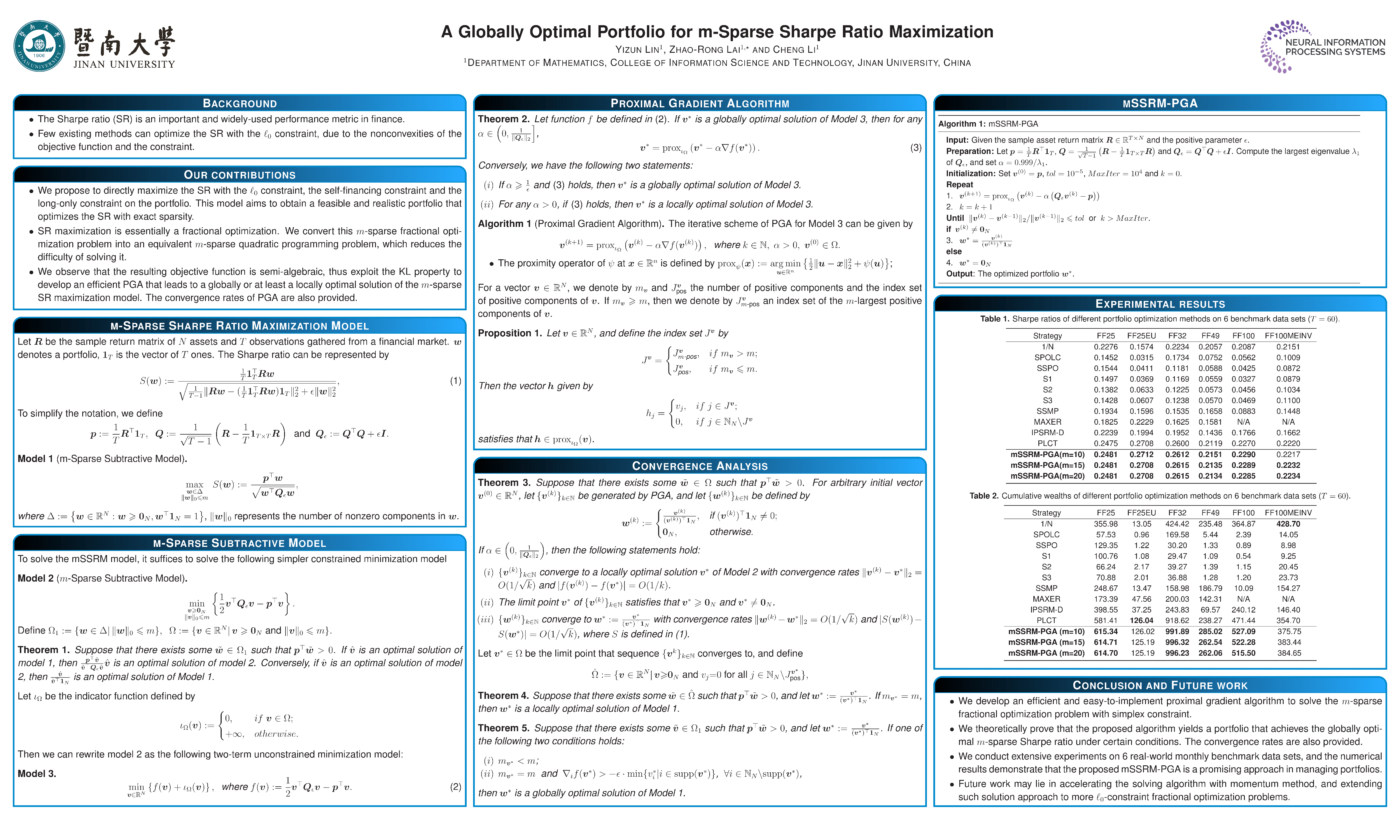

The Sharpe ratio is an important and widely-used risk-adjusted return in financial engineering. In modern portfolio management, one may require an m-sparse (no more than m active assets) portfolio to save managerial and financial costs. However, few existing methods can optimize the Sharpe ratio with the m-sparse constraint, due to the nonconvexity and the complexity of this constraint. We propose to convert the m-sparse fractional optimization problem into an equivalent m-sparse quadratic programming problem. The semi-algebraic property of the resulting objective function allows us to exploit the Kurdyka-Lojasiewicz property to develop an efficient Proximal Gradient Algorithm (PGA) that leads to a portfolio which achieves the globally optimal m-sparse Sharpe ratio under certain conditions. The convergence rates of PGA are also provided. To the best of our knowledge, this is the first proposal that achieves a globally optimal m-sparse Sharpe ratio with a theoretically-sound guarantee.