Poster

in

Workshop: Time Series in the Age of Large Models

Zero shot time series forecasting using Kolgomorov Arnold Networks

Abhiroop Bhattacharya · Nandinee Haq

{kind=link}

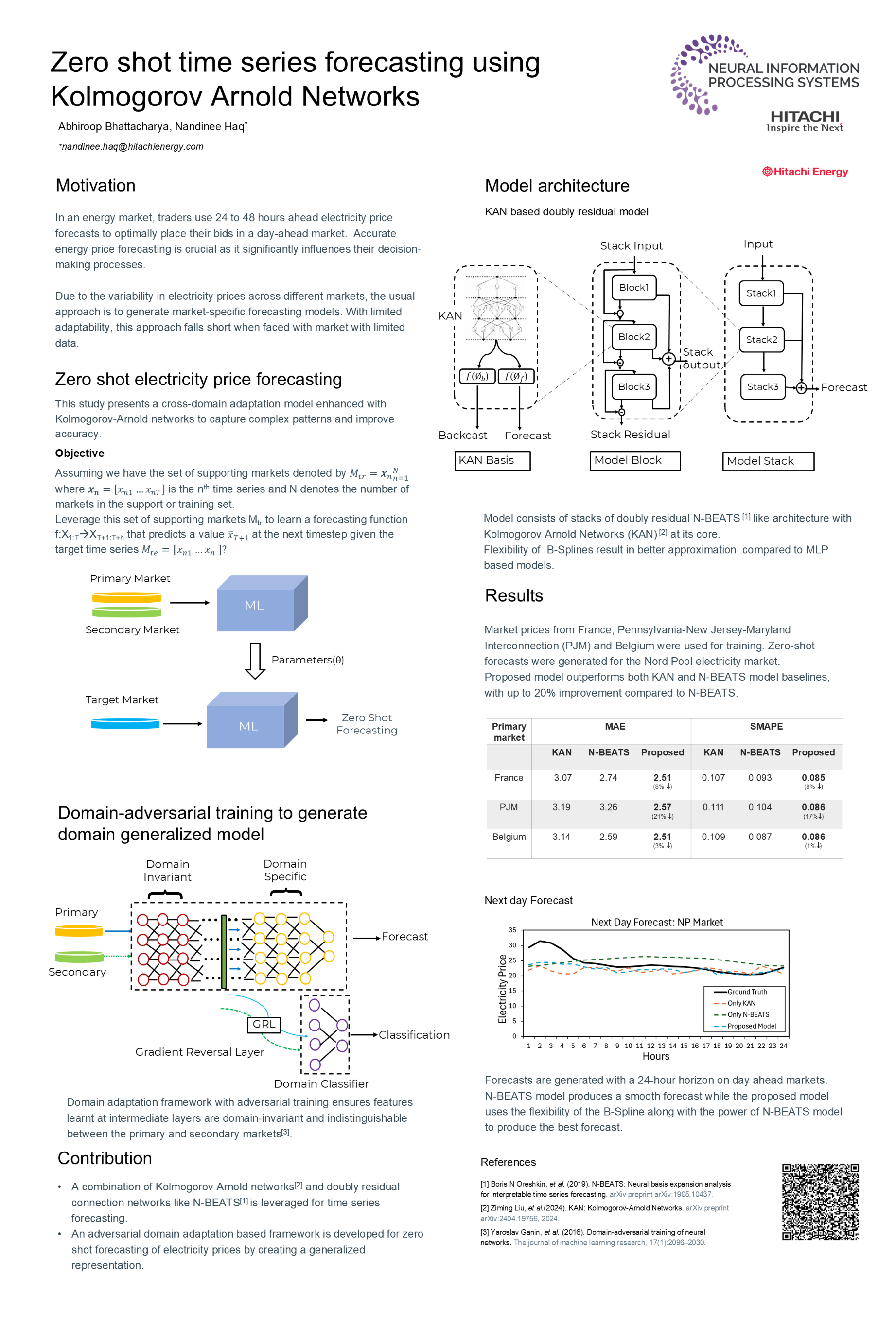

Accurate energy price forecasting is crucial for participants in day-ahead energy markets, as it significantly influences their decision-making processes. While machine learning-based approaches have shown promise in enhancing these forecasts, they often remain confined to the specific markets on which they are trained, thereby limiting their adaptability to new or unseen markets. In this paper, we introduce a cross-domain adaptation model designed to forecast energy prices by learning market-invariant representations across different markets during the training phase. To evaluate the model's effectiveness, we tested its ability to predict day-ahead electricity prices in competitive markets that were not included in the training dataset. Preliminary results indicate that our proposed framework outperforms traditional baseline models. Furthermore, we explore the integration of Kolmogorov-Arnold networks into our forecasting model. These networks, grounded in the Kolmogorov-Arnold representation theorem, offer a powerful way to approximate multivariate continuous functions. By leveraging Kolmogorov-Arnold networks, our model can potentially enhance its ability to capture complex patterns in energy price data, thus improving forecast accuracy across diverse market conditions. This addition not only enriches the model's representational capacity but also contributes to a more robust and flexible forecasting tool adaptable to various energy markets.