Poster

in

Workshop: Agent Learning in Open-Endedness Workshop

Curriculum Learning from Smart Retail Investors: Towards Financial Open-endedness

Kent Wu · Ziyi Xia · Shuaiyu Chen · Xiao-Yang Liu

Keywords: [ financial reinforcement learning ] [ financial applications of open-ended learning systems ] [ quantitative trading ] [ multi-stage training ] [ curriculum learning ]

{kind=link}

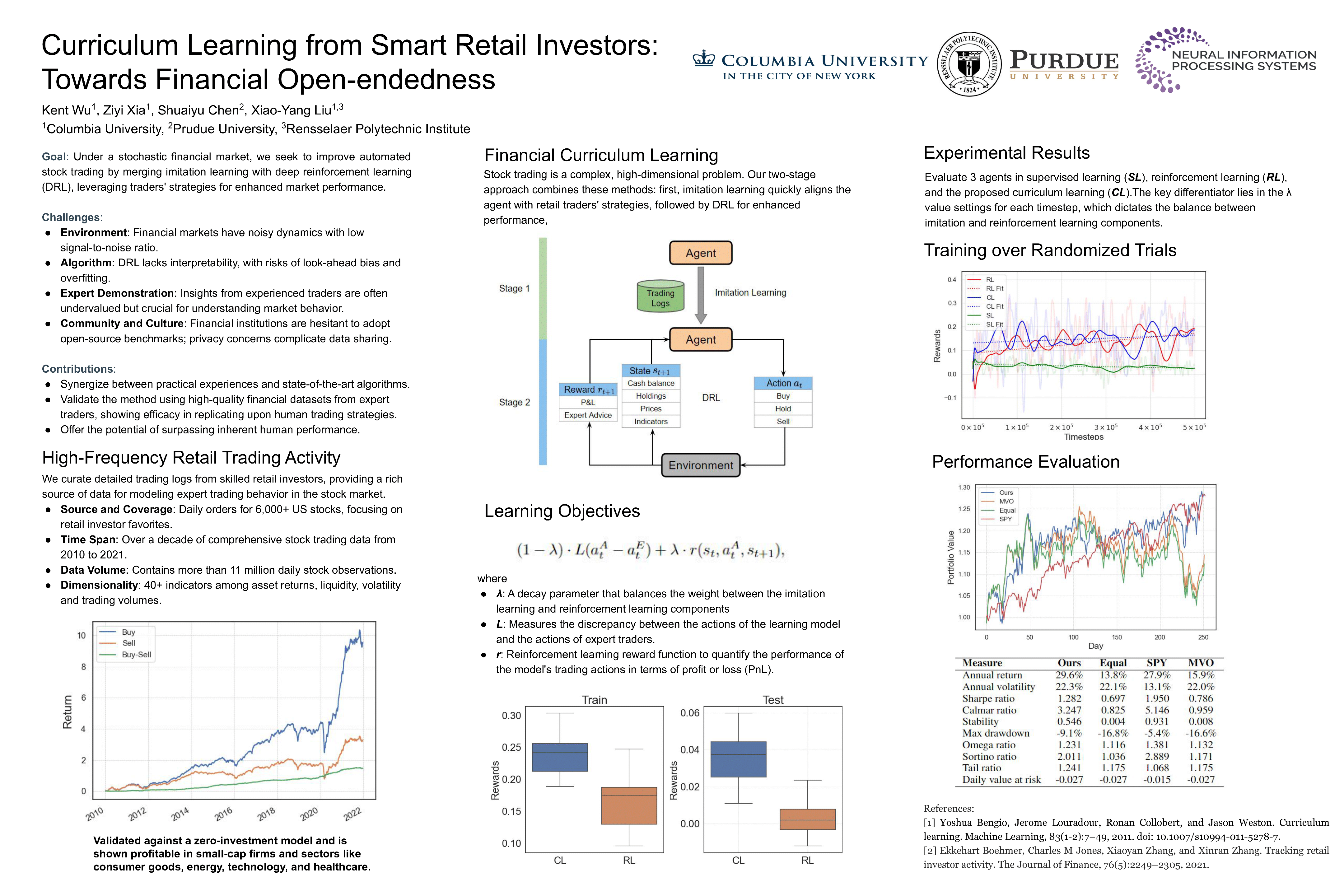

The integration of data-driven supervised learning and reinforcement learning has demonstrated promising potential for stock trading. It has been observed that introducing training examples to a learning algorithm in a meaningful order or sequence, known as curriculum learning, can speed up convergence and yield improved solutions. In this paper, we present a financial curriculum learning method that achieves superhuman performance in automated stock trading. First, with high-quality financial datasets from smart retail investors, such as trading logs, training our algorithm through imitation learning results in a reasonably competent solution. Subsequently, leveraging reinforcement learning techniques in a second stage, we develop a novel curriculum learning strategy that helps traders beat the stock market.